A Nifty 50 (2-yr SIP) XIRR of −1.53% over two years. A G-Sec index at +5.69%. What the data says — and what it doesn’t.

Mobile friendly : http://www.richify.in/perspectives/sip-autopilot-myth-dsk.html

── The Setup ──

The Streetlight Problem

There is an old parable about a drunk man searching for his keys under a streetlight — not because he dropped them there, but because that is where the light is. The SIP is our streetlight. Not because it is always where the answer lies. Because it is the only light most investors know how to turn on.

Over 24 months ending April 2026, a disciplined Nifty 50 SIP returned −1.53% per annum. A 4–8 year government bond index returned +5.69%. That is a 722 basis-point gap — in favour of sovereign paper. No fund manager. No complexity. Just debt. This does not make the SIP wrong. It makes the conversation about when, how much, and at what valuation long overdue.

── Why We Believe ──

Three Truths That Became One Bad Prescription

The SIP narrative rests on three things that are individually correct — and collectively misleading when sold as a single, universal answer.

Rupee-cost averaging works. Fixed monthly investments buy more units when prices fall and fewer when they rise. Over a full cycle, this lowers average cost. Mathematics, not mythology.

Behaviour is the biggest return killer. Study after study shows that the average investor underperforms the average fund — because they buy high and sell low. A SIP removes the trigger finger. That is genuinely valuable.Indian equities compound over long periods. Any 5-year rolling Nifty window from 2006 to 2026 has almost never delivered negative real returns. The statistical backbone is solid.

The problem is the leap — from three correct observations to one sweeping prescription: “Just SIP. Every month. Forever. Don’t think.” That is not investing. That is outsourcing judgment and calling it discipline.

── The Geometry ──

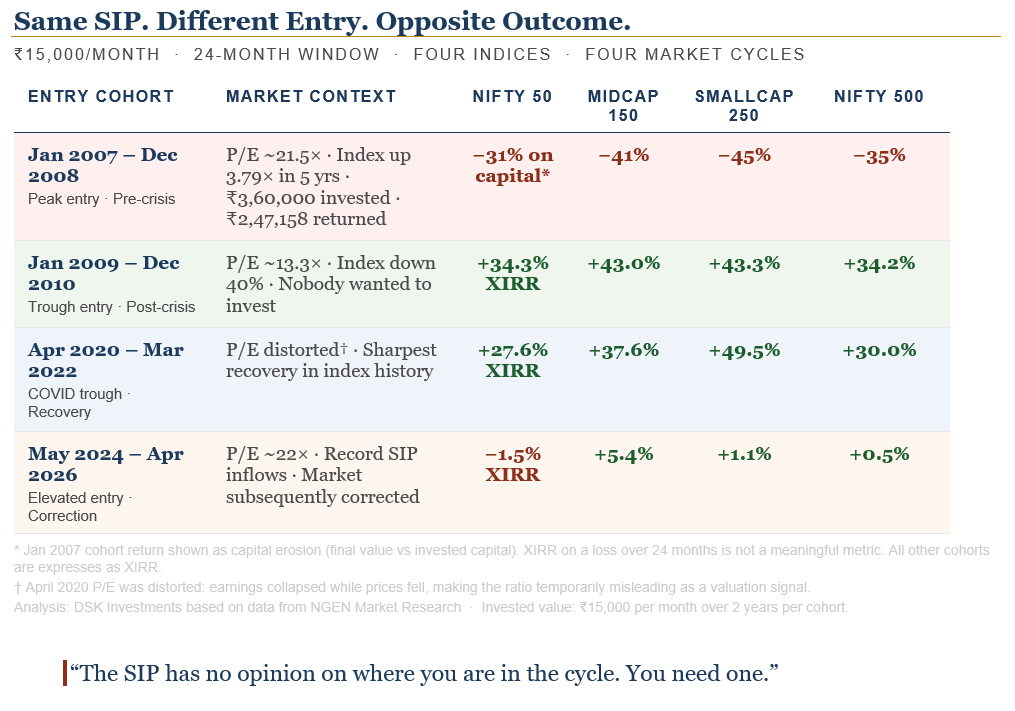

Entry Timing: The Number That Changes Everything

Charlie Munger liked to invert. So: when does a SIP actively work against you? When you start near a peak, in an expensive market, and measure returns before a full cycle completes.

January 2007. Nifty 50 P/E: ~21.5×. Nearly 33% above its prior 5-year average. The index had almost quadrupled in five years. An investor who started SIPing that month recovered — eventually. But measured two years later, in December 2008, the SIP corpus was approximately 31% below invested capital. The mechanism did not fail. The horizon did.

January 2009. Nifty 50 P/E: ~13.3×. The index had corrected 40% from its highs. Nobody wanted to invest. A SIP started that month delivered ~34% XIRR over the following two years. Same instrument. Same discipline. Opposite experience.

── The Cycle ──

Two Years Is Not the Test

The Jan 2007 and Jan 2009 comparison makes a point — but incompletely. Two years is too short a window to judge an equity SIP. The real question is what the full-cycle data says, and critically, what the investor does when their statement looks bad.

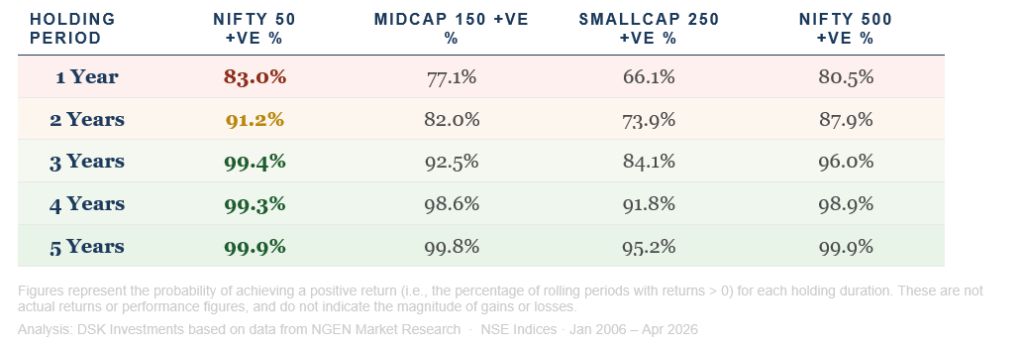

What the Probability Actually Looks Like

Rather than reasoning from selected examples, the rolling return data across every entry point from January 2006 to April 2026 makes the same argument without cherry-picking. The table below shows, for each holding period, what percentage of all rolling windows delivered a positive return — across Nifty 50, Midcap 150, Smallcap 250 and Nifty 500.

The direction is unambiguous. At one year, Nifty 50 SIPs have been positive 83% of the time over this period — but 17% of windows were negative, and those windows include exactly the experience many investors are having today. By three years, that falls to under 1%. By five years, it is effectively zero.

Recovery happens. But the wait for acceptable absolute returns — not just positive ones — has been 3–5 years from peak entries. And each time, investors who entered at elevated valuations arrived with the highest expectations and faced the longest wait to meet even modest returns.

The Industry’s Long-Term Argument — and Its Framing

The standard rebuttal to SIP scepticism is a chart. Twenty-year returns. “In the long run, equity always wins.” The data is real. The framing is selective — start dates are typically anchored just after major crashes, when the base is low and returns are flattering.

The Jan 2007 and Jan 2009 examples above use the same technique, in both directions. The intent is to sharpen thinking, not to sell an alternative. The advertised version shows only the favourable window. We showed you both.

Long Term Is Not a Number. It Is a Cycle.

The industry says three years because its palatable. Regulators present five-year disclosures to improve context. Academics say 15 years. None are wrong. All are incomplete.

The honest answer is investor specific. Long term is simply the time it takes for your entry to pass through a full market cycle—buying at the peak, accumulating through the decline, and holding until the entire cost-averaged position recovers. Start at reasonable valuations, and this cycle may play out in 3–5 years. Start at stretched valuations—like in September 2024 —and it can take closer to 5 to 7. The SIP does not set this clock. Your entry valuation does.

Three Paths at the Trough

Breaking even at the index level and being meaningfully rewarded are not the same event. The recovery gets you back to zero. The reward comes later. That gap in between is where most investors lose patience—and make their permanent errors. In that phase, behaviour matters more than any market variable. When the statement still looks disappointing, three paths emerge:

Keeps SIPing. Buys the cheapest units of the entire tenure at the moment the market feels most dangerous. Each instalment in a falling market does more work than one in a rising market. When the recovery comes, that cheap inventory lifts the entire portfolio—including the expensive early units—through a lower blended cost.

Stops. Paid full price for months of units, then opted out of the discount. Will recover — but more slowly, with a higher cost basis that takes longer to overcome.

Sells. Converts a temporary mark-to-market loss into a permanent one. The SIP did not fail this investor. They exited the only mechanism working in their favour — at the precisely moment it was working hardest.

── The Behaviour ──

The Itch to Act — and the Discipline of Waiting

There is a less-discussed reason the SIP has become the default: it satisfies the need to do something. Money sitting in a liquid fund, waiting for a better entry point, feels like waste — like indiscipline dressed up as prudence. The market goes up. You are not fully in it. The discomfort is real.

The SIP resolves this discomfort. A monthly debit confirmation. Units in the portfolio. The sensation of being a responsible, forward-thinking investor. That psychological function is not trivial. But it can be manufactured more cheaply than most investors realise.

A SIP into a liquid fund or short-duration G-Sec fund preserves the ritual — the automation, the monthly discipline, the habit — while keeping dry powder available for deployment when valuations justify it. The need to act can be satisfied without deploying into an expensive equity market.

The Dry Powder Problem

Position sizing is the dimension almost no SIP discussion includes.

An investor who deploys their entire lump sum via an STP over 12–18 months arrives fully invested when the window closes. If the market then corrects 30%, there is no fresh capital to deploy. The mechanism used to enter has simultaneously exhausted the reservoir needed to exploit the dislocation.

The same trap closes on SIP investors who have stretched to their last deployable rupee. At exactly the point when the market offers the best unit prices of the cycle, they have no slack to increase. Some are stopping entirely — overwhelmed by paper losses. The market is running a clearance sale. Their wallets are empty.

That discomfort—the feeling of sitting on uninvested capital—wasn’t inefficiency. It was optionality. Investors who carried dry powder through the bull phase weren’t idle; they were preserving the ability to act. When the cycle turns, that flexibility becomes valuable. The difference only reveals itself at the bottom—when prices are attractive, but only some investors still have the capacity to respond.

── The Framework ──

The SIP Is a Mechanism, Not a Strategy

Three modes suit three different investor situations. The discipline required is identical. What differs is the awareness brought to it.

| AUTOPILOT For early savers with a corpus under ₹25L, limited market knowledge, and a 15+ year horizon. Fix the amount, fix the date, do not touch it. The discipline alone justifies the approach. |

| VALUATION-AWARE For mid-sized investors (₹2Cr–₹10Cr). Keep the SIP running, but add a volume dial Scale contributions relative to how far valuations sit from their long-term average—trim when markets are meaningfully above trend, and step up when they fall meaningfully below it. This is not market timing. It’s responding to starting conditions. |

| CYCLE-ACTIVE For HNIs (₹10Cr–₹200Cr+). For larger, advised portfolios: think beyond SIPs. You’re managing an existing pool of capital, ongoing surplus, and intermittent inflows—all sitting at different points in the cycle. Use SIPs as a base for incremental cash flows, but actively calibrate overall exposure. Add meaningfully during dislocations, slow or pause incremental deployment at extremes, and rebalance when allocations drift. Windfalls—ESOPs, bonuses, asset sales, inheritances—are not SIP extensions. They are standalone allocation decisions, made in the context of valuations and current portfolio positioning. |

The Volume Dial — A Quick Reference

| Market Signal | VALUTION REGIME (vs long-term mean) | SIP Action | Signal |

| Deep trough — nobody wants in | ≤ -1.5 to – 2.0 STD DEVIATION (SD) | Accelerate (1.5x- 2.0×) | ● GO |

| Normal market — moderate sentiment | –1.0 to +1.0 SD | Run normally | ● HOLD |

| Elevated — market is a dinner topic | +1.0 to +1.5 SD | Trim (reduce 25-50%) | ● CAUTION |

| Euphoric — SIPs are front-page news | +1.5 to +2.0 SD | Pause incremental lumpsum; continue base SIP. | ● STOP |

| Windfall — ESOP / bonus / inheritance | Any | Separate framework* | ◆ Different Rules |

Analysis: DSK Investments

* Windfall note: Any new capital equal to more than 30% of an existing corpus demands a separate deployment framework — staged over 12–24 months, with valuation overrides. The temperament that built the corpus via SIP is not the tool required to deploy a large lump sum intelligently. These require a different conversation.

── The Honest Answer ──

The SIP Is Not Wrong. It Is Not Enough.

The SIP is not a fraud. It solves a real problem—human behaviour at the point of decision. For the early saver deploying ₹5,000–₹25,000 a month over 15–20 years, it is often the right answer. Don’t overcomplicate it.

The problem begins when it becomes the default answer—for every investor, every rupee, at every point in the cycle. It isn’t.

For larger portfolios, the game changes. When you’re managing ₹5 crore or more, valuation awareness, asset allocation discipline, and the willingness to deploy into discomfort are not optional. That is the job.

The same applies to windfalls—ESOPs, bonuses, asset sales, inheritances. When a single inflow can materially shift your portfolio, it is not a SIP decision. Deploying ₹50 lakhs into the same fund you SIP ₹10,000 into—regardless of where valuations sit—is a category error. The discipline that built the corpus cannot substitute for the judgment required to allocate a large sum.

“Set it and forget it” works – until scale changes the problem. For investors managing meaningful capital, the dial exists. Use it.

At DSK Investment Advisors, asset allocation is guided by a 20+ indicator framework spanning valuation, macro, sentiment, and global signals. No single variable triggers a move. Convergence drives action. If you’re navigating a windfall, a growing corpus, or simply questioning whether your current approach fits this point in the cycle, it’s a conversation worth having.